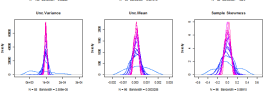

In their paper on GARCH model comparison, Hansen and Lunde (2005) present evidence that among 330 different models, and using daily data on the DM/$ rate and IBM stock returns, no model does significantly better at predicting volatility (based on a … [Continue reading]